Commercial Real Estate News

Commercial Lending Dampened in 2023 by U.S. Market Uncertainty

According to the latest research from CBRE, U.S. commercial real estate lending slowed in the second quarter of 2023 as market uncertainty weighed on available debt capital.

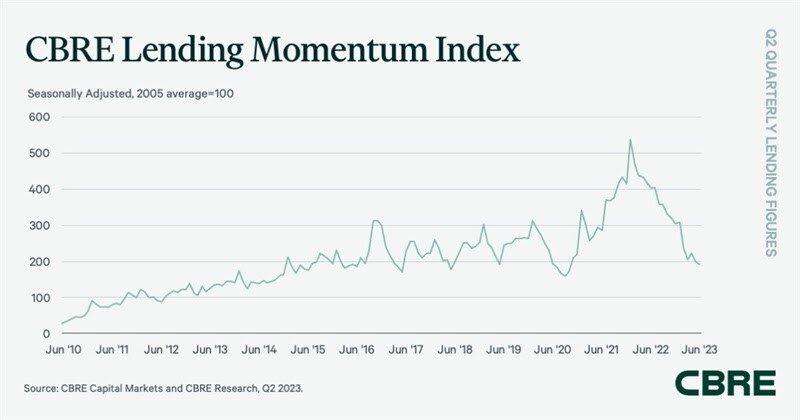

The CBRE Lending Momentum Index, which tracks the pace of CBRE-originated commercial loan closings in the U.S., declined by 5.4% from Q1 2023 and 52.2% when compared with the strong loan volume of a year earlier. The index closed Q2 2023 at a value of 193.

"Despite ample available debt, commercial lending has been hampered by choppy markets," said Rachel Vinson, President of Debt & Structured Finance, U.S. for Capital Markets at CBRE. "Borrowers who have to transact in the current environment are turning to shorter-term fixed loans until stability returns. Costlier credit with tighter terms continues to encourage many to sit on the sidelines."

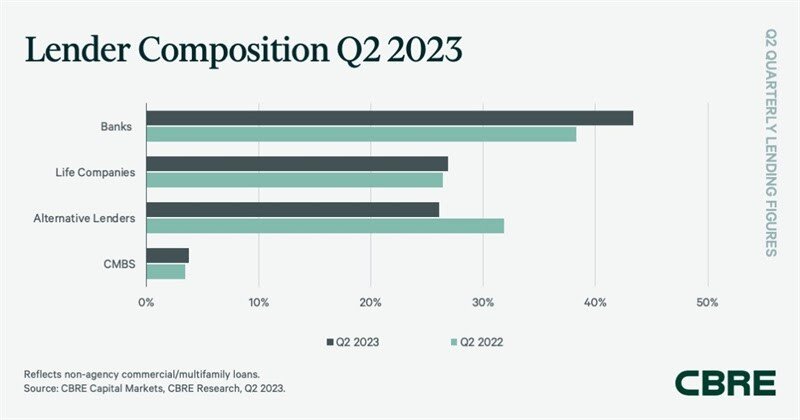

Banks accounted for the largest share of CBRE's non-agency loan closings for the fifth consecutive quarter, with 43.4% of the total in Q2 2023, up from 41% in Q1 2023. Smaller regional and local banks were the most active in this space, with 25% of bank loans used to fund construction projects, mostly in the industrial sector. Approximately 43% of the loans were refinancings, while the remainder was allocated for acquisition loans.

Life companies accounted for 26.8% of closed non-agency loans, up from 23% in Q1 2023, focused on permanent multifamily and industrial loans.

Alternative lenders, such as debt funds and mortgage REITs, took 26% of Q2 2023 closings, up from 20.1% in Q1 2023, but faced challenges on floating-rate bridge loans amid wider spreads and interest rate cap costs. Collateralized loan obligations (CLO) totaled just $2.1 billion in H1 2023, versus nearly $24 billion in H1 2022.

CMBS conduit lending shrank to 3.8% of non-agency loan volume in Q2 2023, down from 15.7% in Q1 2023. Industrywide CMBS origination reached $16.5 billion in H1 2023, down from $49.9 billion in H1 2022.

Underwriting criteria remained tight in Q2 2023, with slightly lower underwritten cap rates, debt yields and interest rates than last quarter. Compared to a year earlier, the average underwritten cap rate increased by 43 basis points (bps) in Q2 2023 to 5.52%, and average loan constants rose to 6.61%, up from 5.43% a year earlier.

Government agency lending on multifamily assets totaled $27.8 billion in Q2 2023, down from $33.4 billion in Q2 2022.

CBRE's Agency Pricing Index, reflecting average fixed agency mortgage rates on 7-10 year permanent loans, rose 9 bps in Q2 2023 and 154 bps year-over-year to 5.41%.